The world of lending is constantly changing - that is no secret. It has already been reported that in the UK, alternative lending by challenger banks now represents 55% of all the SME financing, making alternative funding the new standard. Continental Europe is following the same trend - the emergence of new financing models, such as revenue-based financing, spells out a new era of business funding.

The history of lending

So, what is the history of lending - and why do we call neolending, data-driven financing that Silvr enables, the 3rd generation of lending? Our CEO Nima Karimi had a chance to tell more about why 2023 is such an important year for lending in his speech at Frankfurt Digital Finance:

Balance sheet based lending

The first generation of financiers are banks that have a patrimonial approach: they finance businesses based on their balance sheets. “I call it financing the past, because you’re financing what already happened,” - says Nima. Today’s companies do not have big balance sheets - they may show great potential, but might not be able to come up with a necessary track record to be trusted by legacy banking institutions.

Asset based lending

In the mid-80s, a new form of lending emerged - asset based lending. Here, banks are securing the loan with liabilities - physical assets or properties that you already own. “Factoring companies that finance invoices or leasing companies that finance machines are good examples,” says Nima Karimi. “This is financing what you have just sold or financing what you have just bought - in other words, financing the present.” The new digital businesses are asset-light, which means they aren’t suited for this type of debt either.

Enter the new era of neolending

If the 1st generation of lending was financing the past, and the 2nd generation - financing the present, then how can the 3rd generation of lending finance the future?

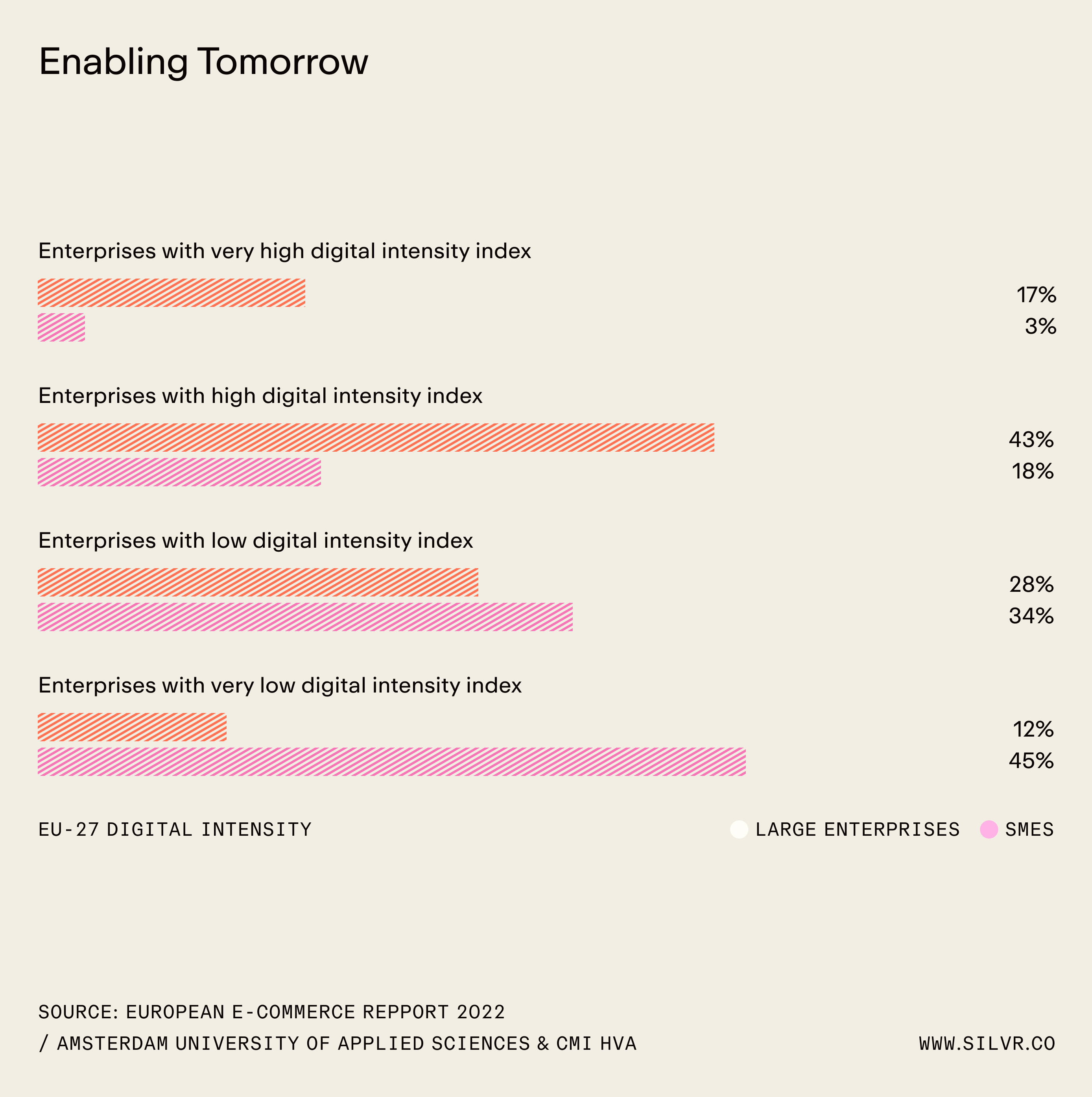

The answer is data. As payments have gradually moved online - more non-falsifiable real-time data is being created within digital businesses every day. They collect payments via PayPal and Stripe, they sell via Amazon or Shopify, they advertise on Google… Neolenders such as Silvr rely on the increasing accessibility of this online data in order to predict the future behavior of companies. These companies, often SMBs, might not have many assets or a long track record - but they show strong growth and great future potential. “We finance against this potential future, because our models can predict the future by analyzing real-time business data,” Nima explains.

Neolending: new funding model for digital companies of today

We sure saw the change that the neobanking wave has brought onto the financial industry. But why is neolending going to be the next one disrupting it in 2023?

A user-centric model

In order to fund digital businesses, you need to understand their business models on a fundamental level. “You need to understand that sometimes, it’s good to invest in a TikTok campaign, because it generates revenue.” This is something that an incumbent lending institution would consider a risky investment - but at Silvr, we can estimate the return of such investments.

Data-based underwriting

“To finance digital businesses the right way, you have to speak their language,” shares Nima Karimi. Data-based underwriting is the best-suited solution for today’s businesses, because neolenders like Silvr speak the language of the business. Today, that language isn’t excel spreadsheets or printed bank statements - it’s real-time cashflow, payment, order data. Connecting to that data via APIs allow instant business performance analysis - that is why our customers find that getting a loan can happen as fast as 24 hours, and refinancing repeatedly is a lot easier.

Modular offering

Loan is not just a monetary amount - it is a complex bundle of conditions, covenants, clauses attached; it is also about how the money is provided, the speed, the service. In creating the best overall service, transparency is key: when businesses apply for funding and connect to Silvr, nothing is hidden. Based on the real-time data, we can provide the best modular loan repayment conditions that are most-suited to a particular cash-flow situation. Neolenders serve businesses as they go… and as they grow.

How does neolending enable the businesses of tomorrow?

In Europe, more than 10 000 companies rely on the digital ecosystem. Only the top 1% of the 1% will ever end up in the eye and the portfolio of a VC fund. But great businesses deserve to grow, even if they’re not the future unicorn.

In addition to that - even the non-digital businesses of the past are rapidly getting digitized. Nima takes the example: “even the baker at the corner of your street is starting to use software to collect their payments and engage with their clients.”

So when we talk about neolending - we don’t just mean funding for digital-only entrepreneurs; we mean financing the whole economy that is gradually digitizing, and is in need of the appropriate funding tools.

Would you like to get your businesses to the next milestone? Try the first European neolender here and receive the capital your business needs to grow today.